A new report by Northwestern University in Qatar (NU-Q), in partnership with the Doha Film Institute (DFI), points to shifts in regional media offerings of the Middle East. In the past the region’s media landscape was often associated with limited offerings and stagnation.

This report shows that an expansion of media channels and content has occurred coming from a wider and more diverse range of sources, including local and international players not usually associated with this industry in the Middle East.

The region-wide study, Media Industries in the Middle East, 2016, points to a general expansion of channels and offerings across all sectors, including broadcast, print, and digital media. The new content also tends to represent a wider variety, created by a broader diversity of content producers.

Previous research had suggested that regional audiences are both hungry for content reflecting their own culture and are generally open to media from other parts of the world; however, they had been limited by the mass-market options available to them.

The recent expansion of channels and offerings is obviously diminishing the disconnect between what audiences in the Middle East want and the media they can access.

“Similar to the media use survey, which NU-Q conducts annually,” Everette E. Dennis, dean and CEO of Northwestern University in Qatar, said, “today’s report on the media industry provides additional resources to understand the media landscape in this region. Over the past several years, NU-Q has been building a body of research that takes a keen look at media and entertainment consumption in the region. This most recent collaboration with the Doha Film Institute is an opportunity to look at the other side of the equation: the organizations and businesses that produce and distribute content.”

Doha Film Institute Chief Executive Officer Fatma Al Remaihi said: “Our most recent collaboration with NU-Q has produced a significant piece of research that presents new and informative insights on the regional media landscape which will bring tremendous value to the industry. At the Doha Film Institute, we have been strong advocates for promoting Arab voices through the medium of film. It is heartening to see from the study that the emergence of new systems, entities and collaborations across the region has contributed to an increase in the number of films being produced. It is imperative that we sustain this momentum through more co-productions and joint venture initiatives to meet the growing appetite for Arab content in the region.”

NU-Q and DFI initiated the project last spring, leveraging the access to unique data, contacts, and experience at the two organizations. Project authors, NU-Q’s Klaus Schoenbach and Robb Wood, supported by recent NU-Q alum Marium Saeed, assembled a wide-ranging team of contributors from Northwestern faculty, Doha Film Institute staff, and ten contributing “expert commentators” from across the region and world. A team from Monitor Deloitte, known for its expertise and extensive contacts in the media sector, was brought on board the project to collect and assess industry data as well as gather information from a program of nearly 100 interviews with industry insiders. The team also contributed to insights and analysis.

Some highlights of the findings:

FILM

- In two of the biggest MENA cinema markets – Lebanon and Egypt – Arabic-language films earned more at the box office per title than non-Arabic films. This is despite Arabic-language films claiming only a fraction of box office revenues overall throughout the region.

- While Egyptian films claimed nearly all box office revenues among Arabic-language films in Egypt and UAE since 2012, Lebanese films have made nearly two-thirds of box office revenues in their own country over the same period.

- Analysis of previously unreleased data compiled by the Doha Film Institute reveals a robust independent film scene in the Arab World, which reflects far greater diversity than the relatively homogeneous mainstream cinema that has been the custom in the Middle East:

- Independent films are twice as likely to have female directors and originate in a far wider range of countries than their mainstream cinema counterparts.

- Egypt is not only home to “commercial” mainstream films. Egyptians are also the most common nationality overall among writers, directors, and producers of independent film.

- France plays a central role in independent Arab film - far more than any other country outside the region.

- The most common nationality of writers and directors of higher-budget independent films is Lebanese.

ADVERTISING

- Release of advertising market estimates based on newly updated industry data show the regional market holding steady through the recent years of social turmoil, with a total value in 2015 of just over USD 5.5 billion. UAE edged out Saudi Arabia as the largest national advertising market, at USD 632 million (excluding Pan-Arab revenues).

- Gains in television and digital advertising have largely made up for losses in newspapers and magazines.

DIGITAL MEDIA

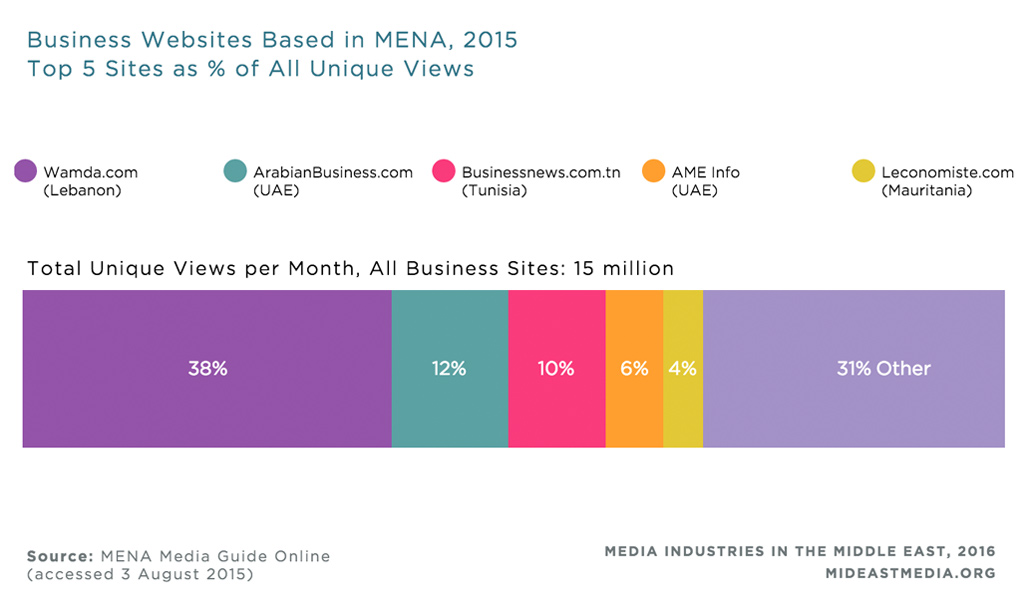

- Has the Arab world skipped the website age and gone social? Compared to the total population of Arabic speakers, there is a disproportionately low number of Arabic language websites, but a disproportionately high number of the world’s top Facebook pages, Twitter accounts, and YouTube channels in Arabic.

- According to extensive industry interviews, digital advertising is more common in the region than reported by major tracking agencies, but is still a small portion of total advertising revenues compared to many other parts of the world.

TELEVISION

- There was a sharp rise in the number of TV channels available in the region in the years after 2012, while advertising revenues have remained relatively flat.

- More non-scripted shows are appearing on the major channel lineups, and more of those are made in Arab countries.

RELIGIOUS TELEVISION

- The number of religious free-to-air television channels grew by fifty percent in the three years between 2011 and 2014, at the same rate as free-to-air channels overall.

- While the majority of religious channels in the region remain Sunni-affiliated, Shia and Christian channels have more than doubled since 2011.

NEWSPAPERS

- Newspaper advertising revenues have declined by a fifth since 2010, but circulation has remained fairly stable.

- Newspapers still claim a substantial share of overall ad spend in national markets, benefitting from their well-defined national distribution areas.

MAGAZINES

- Similar to newspapers, region-wide magazine advertising revenues have dropped by 25 percent since 2010, but overall circulation has remained steady.

- 90 percent of the revenue of MENA magazines comes from ads. As a point of comparison, in the U.S. that number is closer to one-third.

MUSIC

- The music industry is grappling not only with challenges common worldwide, but also struggling to develop viable online options due to rampant piracy, low credit card penetration, and a limited performance rights tracking infrastructure.

RADIO

- Radio still claims only around three percent of total advertising revenues in MENA, considerably lower than in other parts of the world. But, compared to other world regions, where radio’s share of ad revenues has decreased somewhat since 2010, it has remained relatively stable or even increased slightly in the MENA countries.